There Was No Noticeable Increase In Demand For North America Construction

Framing Dimension Softwood Lumber In The Middle Of April.

Demand remained muted as customers felt only more cautious about external

factors like macro-economic conditions and skyrocketing fuel prices. Sellers

responded by continuing to keep their sold wood inventories low, as

confusion reigned and no one wanted to get stuck with high-cost material if

prices fall.

Concern about having to fill inventory holes with material at

below-replacement costs was on the top of everyone’s minds.

As in 2025, the instant snow melted wildfires started. Indeed, British

Columbia already put in a fire ban at the end of April. Sawmills had spent

the winter focussed on timber harvest, so operators were well loaded up with

fibre in their log yards.

Whenever proper demand does arrive, lumber producers will be able to

increase production to meet that. If business continues slow, sawmills will

remain in curtailment / downtime.

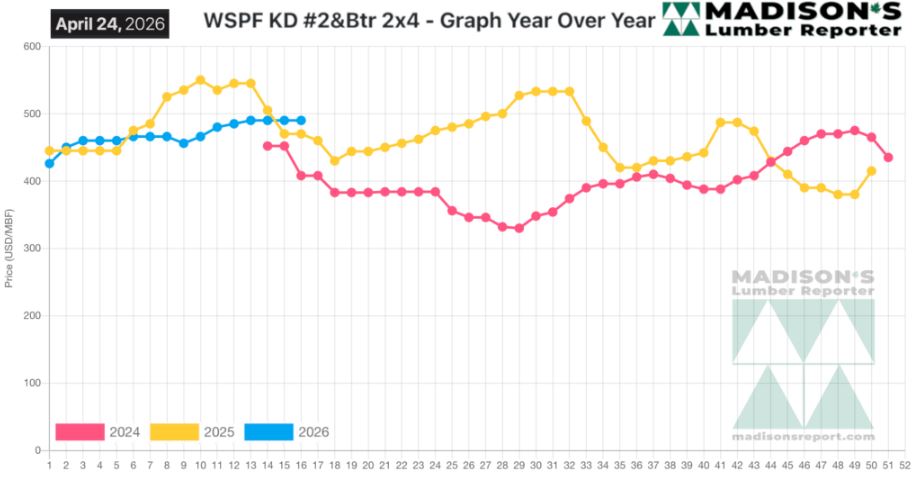

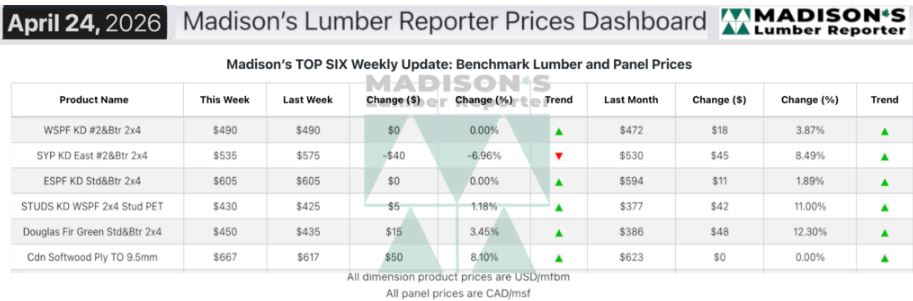

In the week ending April 24, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$490 mfbm.

This was flat from the previous week, said weekly forest products industry

price guide newsletter Madison’s Lumber Reporter.

That week’s price was up +$18, or +4%, from one month ago when it was $472.

Compared to the same week last year, when it was us$470 mfbm, the price of

western spruce-pine-fir 2×4 #2&btr kd (rl) for the week ending April 24,

2026 was up +$20, or +4%.

Compared to two years ago when it was $408, that week’s price was up +$82,

or +20%.

Lumber demand continued to be broadly supply-driven, with limited

availability propping up prices even as many buyers took the week to step

back, digest, and reassess.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Western-SPF suppliers in the US were busy enough that they were running out

of wood.

Producers were, at best, selling just around production costs.

In Canada, Western-SPF sawmill prices continued to level off.

Elevated fuel prices and unpredictable shipping timelines added complexity

to an already-tricky shipping equation.

Sawmill order files were maintained around two- to three-weeks out.

The Eastern-SPF market was signified by a notable lack of optimism.

Distributors were busy as buyers did everything possible to avoid building

inventory.

Purveyors of Southern Yellow Pine contended with a confusing market as mixed

signals alternately indicated firmness or vulnerability.

Eastern Stocking Wholesalers in the US Northeast had to be nimble as they

avoided carrying even a scrap of excess inventory.

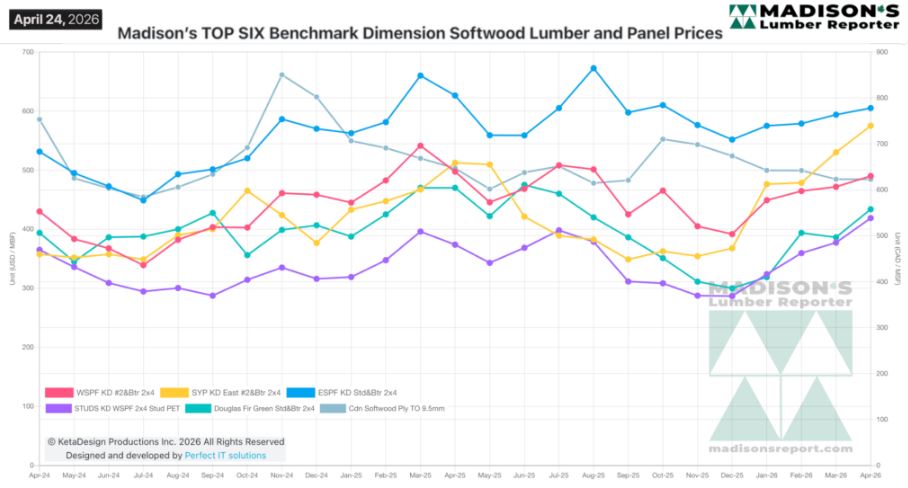

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: