Japan

Wood Products Prices

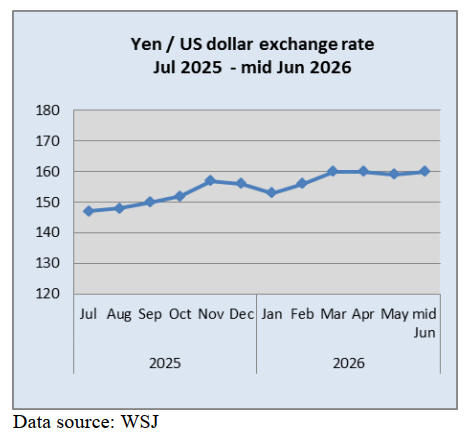

Dollar Exchange Rates of 10th

June

2026

Japan Yen 160.22

Reports From Japan

Bank of Japan discusses interest rate increase

The Bank of Japan (BoJ) is set to raise its key interest rate

to 1.0% from the current 0.75% at its policy board meeting

on 15 and 16 June as the Japanese economy faces upside

risks of inflations. The BoJ is also considering pausing the

tapering of its government bond purchasing program,

starting in April 2027.

"Even if the situation remains unclear, should it be judged

that upside risks to prices outweigh downside risks to

economic activity, it will be necessary to thoroughly

discuss the pros and cons of raising the policy interest

rate," said Kazuo Ueda, Governor of the BoJ

He also said that the BoJ should discuss raising rates if

inflation outweighs concerns about an economic

slowdown, suggesting it could proceed with a rate hike

despite the ongoing Middle East uncertainty.

According to BoJ data released last month, Japan’s

Corporate Goods Price Index for April rose 4.9% year on

year, marking the highest growth since May 2023.

If the BoJ falls behind in raising interest rates, rising prices

at the corporate level could spread, potentially accelerating

increases in the consumer price index.

A weak yen and higher crude oil prices driven by Middle

East tensions are pushing up import costs. Businesses are

becoming more aggressive in passing these costs onto

consumers, potentially causing underlying inflation to

exceed projections

While the Middle East conflict and geopolitical trade

scenarios remain key sources of uncertainty, hawkish BoJ

board members argue that keeping real interest rates

deeply negative poses a larger long-term risk to the

economy. Ahead of the June meeting, analysts see a high

probability of a rate hike as the BOJ continues its

normalisation path.

Upturn in Japanese household spending on furniture

According to the Ministry of Internal Affairs and

Communications household spending in Japan dropped

0.5% YoY in April 2026, easing from a 2.9% decline in

March and beating market expectations for a 1.5% fall.

While this marked the fifth straight month of contraction,

it was also the mildest decline suggesting that easing

inflationary pressures may be helping to support consumer

spending.

Expenditure on food fell at a slower pace, (-0.5% vs -2.9%

in March) while spending increased for transport and

communication (7.5% vs -16.8%), housing (7.6% vs

15.3%), furniture and household goods (19.0% vs 5.5%),

healthcare (6.7% vs 20.1%) and culture and recreation

(6.3% vs 4.6%).

Pledge to cut consumption tax but challenges remain

The government is considering lowering the consumption

tax rate on food to 1% for two years from next April. The

election pledge was for a zero rate but major cash register

system vendors have said that it would take around one

year to adjust systems for a zero percent consumption tax

rate, but only around half a year for a 1% tax rate.

While there is growing support for modifying the election

pledge in order to tackle rising consumer prices swiftly

even the 1% option would present challenges, especially in

securing about yen 4 trillion in annual funding for the tax

cut. The domestic media has reported that the government

may spend about yen 600 billion on subsidies for updating

cash registers.

According to a Mitsubishi Research Institute report a

consumption tax cut on food could hurts small farmers

because their outgoing costs for farming supplies remain

highly taxed, while the tax revenue they collect on the

food they sell drops. Because many small farms are

exempt from remitting consumption tax to the

government, a rate reduction will erode margins.

See:

https://www.japantimes.co.jp/news/2026/06/02/japan/takaichi-

food-tax-one-percent/

and

https://mainichi.jp/english/articles/20260614/p2g/00m/0na/00200

0c

Yen weakness reflects domestic conditions

The yen remains weak due to a combination of cost-push

inflation, demographic pressures and wide interest rate

differentials with the United States. Sayuri Shirai of Keio

University, writing for the EastAsiaForum says, the yen’s

weakness increasingly reflects domestic conditions. One

key factor is the country’s heavy dependence on imported

energy. Rising oil and gas prices worsen the trade balance

and generate inflationary pressures.

Cost-push inflation suppresses purchasing power and

limits economic momentum. While rising nominal wages

are a positive development they have often lagged behind

increases in food and energy prices, leaving many

households under sustained pressure.

Real income growth remains weak and consumption

continues to recover only gradually. Even when external

pressures ease, there is little domestic support for a

rebound in the yen.

Analysts at Commerzbank note that Japan's structural

economic backdrop is showing clear signs of independent

strength. However, they argue that these domestic

improvements are currently overshadowed in the currency

markets as global commodity fluctuations and

international conflicts remain the primary forces

suppressing the yen's value.

See: https://eastasiaforum.org/2026/06/09/japans-structural-

constraints-reinforce-the-yens-new-normal/

and

See: https://www.tmgm.com/en/analysis/market-

news/article/japanese-yen-outlook-looks-weak-despite-

expectations-of-boj-rate-hike-202606091112

Japan’s real estate paradox

Japan is facing a real estate paradox defined by a chronic

oversupply of roughly 9 million abandoned homes (known

as akiya) in rural and suburban areas, paired with surging,

record-high, residential prices and bubble-risk concerns in

metropolitan hubs like Tokyo.

Unlike the housing crises in the US or Europe that stem

from inventory shortages, Japan struggles with an excess

of supply.

This issue is fueled by a shrinking, rapidly aging

population and a cultural reluctance to buy older

properties. Furthermore, tax incentives frequently

encourage property owners to build new houses on

inherited land rather than tearing down or selling old ones.

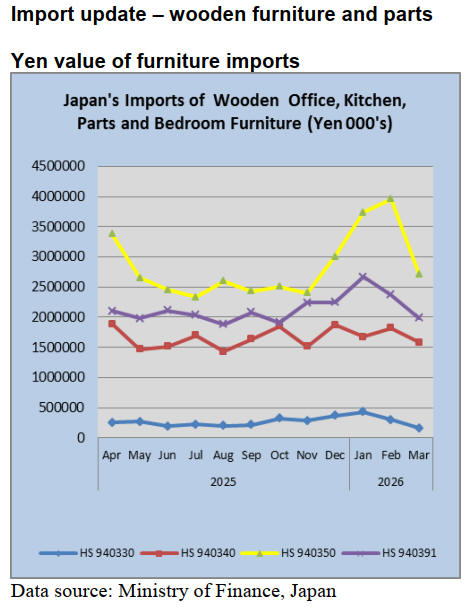

March 2026 wooden office furniture imports

(HS940330)

The top suppliers of wooden office furniture (HS940330)

in March 2026 were manufacturers in China, accounting

for 89% (86% in February) of imports. The other two main

suppliers were from makers in Viet Nam and Malaysia.

The top three shippers accounted for over 90% of Japan’s

March 2026 imports of wooden office furniture.

Surprisingly, there were no arrivals of HS940330 in March

from shippers in Europe with Turkey and the US being the

only non-Asian suppliers.

The value of March 2026 imports of HS940330 was down

46% from February and down 39% from March 2025. The

value of March imports from both Viet Nam and Malaysia

were down compared to that reported for February. The

decline in the value of March 2026 imports added to the

decline observed in February.

March 2026 wooden kitchen furniture imports

(HS940340)

Year on year the value of March wooden kitchen furniture

imports was down 13% and compared to February the

value of imports lower by 10%.

In March 2026, the top two shippers of wooden kitchen

furniture (HS940340) were the Philippines and Viet Nam.

These two countries accounted for over 80% of Japan’s

imports of wooden kitchen furniture in March.

The value of shipments from the Philippines in March was

the highest, accounting for 51% (49% in February) of the

total value of shipments of wooden kitchen furniture. The

other main supplier, Viet Nam, accounted for 31% (29%

in February) of the value of March imports.

The value of March shipments from the Philippines was

down month on month as was the value of shipments from

Viet Nam. The value of March arrivals from Shippers in

China was down month on month with only arrivals from

Malaysia posting month on month gains.

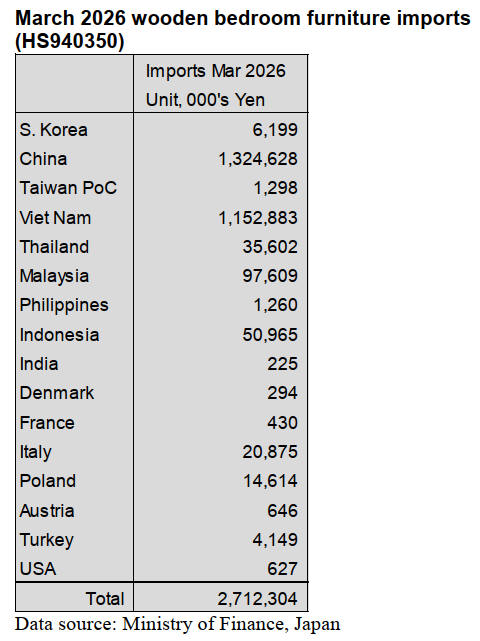

March 2026 wooden bedroom furniture imports

(HS940350)

The upward trend in the value of wooden bedroom

furniture (HS9403550), which began at the end of 2025,

ended abruptly in March. The value of March imports was

31% below that of February and 27% below that of March

2025. The value of March shipments from all four main

suppliers dropped when compared to a month earlier.

Four countries accounted for 94% of the value of

HS940350 imports in March, China, 44% (58% in

February), Viet Nam 43% (36% in February) and

Malaysia along with Indonesia. The other significant

suppliers of wooden bedroom furniture to Japan in March

were Thailand and Italy.

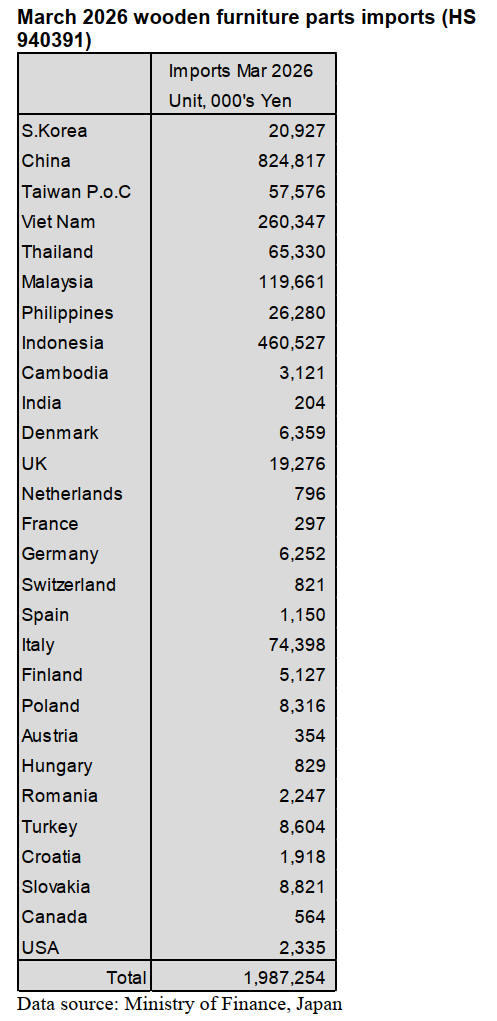

March2026 wooden furniture parts imports

(HS940391)

Shippers in China and three SE Asian countries, Viet

Nam, Indonesia and Malaysia accounted for 84% (90% in

February) of Japan’s imports of wooden furniture parts

(HS940391) in March 2026.

The main shipper of wooden furniture parts in March was

China at 42% (55% in February) followed by Indonesia at

23% (13% in February), Viet Nam 13% (16% in February)

and Malaysia 6% (6% in February). Of the non-Asian

suppliers arrivals of wooden furniture parts from Italy and

the UK were notable.

The value of arrivals of HS940391 in March was 16%

lower than in February 2026 and 10% lower than in March

2025.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

Japan’s lumber exports to US rebound

Japan’s lumber export statistics for March show that

shipments of sawn timber to the United States reached

7,207 cbms, surpassing the 7,000-cubic-metere mark for

the first time since June 2021. Since 2018, this represents

the second-highest monthly volume, following the 7,260

cbms recorded in March 2021, when exports of Japanese

cedar fencing and decking materials were particularly

strong.

Amid a slowdown in shipments of Japanese cedar lumber

from China to the United States due to Trump-era tariffs,

exports from Japan to the U.S. have continued to rise since

last year.

Exports of sawn timber to the United States gained

attention particularly for Japanese cedar fencing and

decking materials, as supplies of Western Red Cedar,

traditionally used for exterior applications in the U.S

declined. Supported by rising prices and increased stay-at-

home demand during the COVID-19 pandemic, shipments

began climbing in the latter half of 2020. Annual volumes,

which had previously remained in the 20,000-cbm range,

exceeded 50,000 cbms in both 2020 and 2021.

However, exports retreated in 2023–24 to the 30,000–

40,000-cbm range, as U.S.-bound shipments of cedar

fencing and decking produced in China—using Japanese

cedar logs exported there— expanded, and inventories of

exterior-use lumber increased within the United States.

In 2025, however, exports rebounded to 58,246 cbms,

supported by the lighter tariff burden on shipments from

Japan compared with those from China, as well as by the

weaker yen.

During the January–March period of 2026, total log

exports reached 469,840 cbms, down 5% from a year

earlier. Shipments to China—which account for roughly

90% of the total—also edged down slightly but remained

at the second-highest level since 2018, following last year.

Meanwhile, cumulative sawn timber exports for January–

March totaled 47,540 cbms, up 12% from a year earlier.

While shipments to China fell 20% to 12,517 cbms,

exports to the United States surged 42% to 16,970 cbms,

driving overall growth. Looking ahead, rising prices in the

United States— partly influenced by instability in the

Middle East—could begin to affect the market.

National forests could resume market stabilising role

The Forestry Agency’s National Forest Management

Department has announced its major project plans for

fiscal 2026.

Despite noting significant uncertainties stemming from the

situation in the Middle East and fluctuations in timber

supply and demand, the agency set its targets at a 2% year-

on-year increase in standing timber sales and the same

volume as the previous year for log (processed timber)

sales.

Although crude oil prices remain volatile and shortages of

naphtha-related products persist, the agency noted that the

impact on the forestry sector is “not causing any

immediate disruption at this point,” according to the

Planning and Management Division.

However, drawing on the role that national forests played

in stabilising supply and demand during the COVID-19

pandemic and the so-called “wood shock,” the agency said

it will consider taking action depending on how conditions

develop.

Vietnam plywood supply tightens

Delays have begun to surface in shipments of BC-grade

Vietnamese plywood, a key product in the mainstream

packaging segment. In addition to labor shortages

following the Tet holiday, restrictions on adhesive supply

have further constrained production, resulting in shipment

delays of one to two weeks or longer in recent weeks.

With uncertainty over the outlook intensifying and

production costs continuing to rise, domestic sales prices

in Japan are all but certain to climb further.

Procurement of adhesives has emerged as the most

significant bottleneck for Vietnamese plywood and LVL

used in packaging applications. While supply has not been

completely cut off, factories are operating under strict

purchase caps, and inventory levels vary widely from plant

to plant, creating uneven production conditions across the

sector.

Benchmark domestic prices are currently around ¥1,200

per sheet for plywood (4×8 panels, delivered to packaging

plants) and roughly ¥56,000 per sheet for LVL on the

same basis. However, plywood prices are expected to rise

to nearly ¥1,300 per sheet by the end of May as cost

pressures intensify.

Looking ahead, LVL is expected to remain in a high price

range, with lead times lengthening somewhat but overall

supply continuing. Plywood, by contrast, is likely to face a

sharper deterioration in supply conditions, with lower-

priced grades such as BC-grade particularly vulnerable to

further declines in arrivals and worsening delivery delays.

South Sea logs and lumber

Demand for South Sea hardwood products and China-

made materials remains sluggish with deck-related items

also seeing slower movement since the start of the new

fiscal year. In producing regions, log harvesting has stayed

at low levels due to weather and other constraints, and

sawmill operations have not picked up.

Although Japan’s weak domestic demand has limited the

immediate impact, some market participants note concerns

about fuel shortages in Southeast Asia stemming from the

effective closure of the Strait of Hormuz, raising the risk

of prolonged disruption. In the glulam free-board market,

Indonesian merkus pine products continue to command

high prices due to ongoing harvesting restrictions.

Chinese red-pine products, which had previously

maintained stable selling prices, are now also seeing

upward revisions as local manufacturers move to raise

prices. In Japan, with overall market activity stagnant,

buyers remain cautious about placing new orders,

particularly for merkus pine products, whose export prices

were raised in February. Still, as high export prices persist,

domestic prices have begun to rise as well.

For South Sea hardwood logs, higher crude-oil prices have

pushed up harvesting costs for producers, slowing logging

activity.

While Japanese buyers are currently well supplied and

short-term effects are limited, prolonged reductions in

harvesting could eventually affect availability.

|