|

Report from

Europe

EU reviews impact of VPAs and EUTR

On 4 May, the European Commission (EC) published a

comprehensive independent evaluation of the EU FLEGT

Action Plan. The Plan encompasses the wide range of EU

policy measures introduced over the last decade to support

good forest governance and remove illegal wood from

trade.

Key amongst these are the EU Timber Regulation (EUTR)

and the Voluntary Partnership Agreements (VPAs) now

being implemented by six tropical countries and

negotiated by another nine countries. The report assesses

progress since the PlanˇŻs publication in 2003 and makes

recommendations for future action.

The reportˇŻs central conclusions are positive: the EU

FLEGT Action Plan is assessed to be a relevant and

innovative response to the challenge of illegal logging and

to have improved forest governance in all target countries.

The report says the EU FLEGT Action Plan has been

effective in terms of raising awareness of the problem of

illegal logging at all levels, contributing to improved forest

governance globally and particularly in partner producer

countries, and has helped reduce demand for illegal timber

in the EU.

The reportˇŻs recommendations imply that the Plan is

heading in the right direction and not needing a major

overhaul. ˇ°Main pillars and action areas should be

retained, but FLEGT support to producing countries

should be delivered in a more demand-driven and flexible

manner, while bottlenecks affecting VPAs should be

addressed and the private sector more involvedˇ±.

The report suggests that ˇ°the direct FLEGT objective of

decreased EU imports of illegal wood is being achievedˇ±.

This observation is based largely on the results of

interviews and perception surveys undertaken by the

consultants both in the EU and producer countries over the

last two years rather than any direct evidence from

changes in trade flows.

Assessments of trade flows have yet to reveal any

significant step change in trade that can readily attributed

to measures such as the EUTR and VPAs which are

central to the FLEGT Action Plan.

Lack of progress on trade aspects of FLEGT

The report highlights that while the Action Plan is

contributing broadly to its specific objectives, itˇŻs

effectiveness across action areas varies widely. It notes

that progress on trade aspects of the plan has been a

particular area of weakness and that there is a need for

greater focus on VPA and EUTR implementation and

private sector engagement.

The report suggests that the VPA process has yet to

deliver on the Action Plan objective of increasing market

confidence for timber from participating countries. In fact,

interviews in VPA countries as part of the evaluation

indicated that many observers feel that the EU market is

now less confident than before about tropical timber.

To a large extent this failure to increase market confidence

is tied up with the lengthy time between signing a VPA

and delivery of FLEGT licensed timber. The report is

blunt in its assessment of efforts to develop Timber

Legality Assurance Systems (TLAS) noting that

ˇ°generally speaking, the TLAS projects have met with

little successˇ±.

According to the report, out of 200 responses to the Public

Survey, less than 5% consider the TLAS to be a major

achievement of the FLEGT Action Plan.

Furthermore, responses to the VPA-country survey

undertaken by the consultants indicate that countries

implementing a VPA still consider the TLAS to be a

challenge.

The reasons vary from country to country: in Cameroon,

Congo and CAR the Wood Tracking Systems (WTS)

development and acquisition projects have so far been

difficult to manage and expensive; in Vietnam, there have

been disagreements between the partners on approaches to

TLAS development, including the scope of verification; in

Malaysia the need for capacity building to run the TLAS

has been underestimated.

Moreover, VPA countries find it hard to accept the lack of

recognition of their efforts to enhance their broader

governance framework (in the absence of FLEGT licenses

they are treated like any non-VPA country). This has led

several countries (Vietnam, and Congo) to propose a

phased application of the TLAS, while in Cameroon such

is being suggested by stakeholders.

FLEGT licensing in Ghana and Indonesia close to

operational

More positively, the report suggests there is general

recognition that VPA negotiation and implementation,

strongly supported by EFI, the EC and EU Member States,

have helped to sharpen the legality definition, and this has

been valuable, even if no functioning TLAS has been

produced.

The VPA Survey revealed that three VPA implementing

countries acknowledge the positive effect of the legality

definition process on the development of the TLAS. And

despite the challenges, two countries ¨C Ghana and

Indonesia ¨C now have systems very close to operational.

Another observation is that the Action PlanˇŻs contribution

to the objective of sustainable forest management is

unclear and needs to be made more explicit. According to

the report, available data suggest that the TLAS under

development are not necessarily enhancing more

sustainable forest management (SFM) or SFM

certification, and that this is not envisaged by many

stakeholders in VPA countries.

ThereˇŻs also a concern that FLEGT needs to focus more

on domestic timber markets and support for the actors

operating in them. This is seen as critical to the broader

FLEGT objective of contributing to poverty reduction.

Slow EUTR implementation weakens incentives.

Considering the EU demand side, the report echoes many

of the conclusions of the EU review of the EU Timber

Regulation published earlier this year. The report suggests

there is a widespread perception that EUTR has been

implemented slowly and unevenly and that this is

decreasing incentives for VPA countries to commit to

finalising FLEGT licensing systems.

The report notes that ˇ°while advances have been made [on

EUTR implementation], there have been major differences

between front-runner [EU] countries and slow followers.

This has resulted in unfair competition between Member

States, inconsistent market requirements for the private

sector in producer countries and a risk that VPAs would

lose their value and the EC some of its credibilityˇ±.

The report goes on to suggest that the capacity of most

EUTR authorities is considered rather limited, in terms of

staff numbers, budgets and training. In important timberimporting

countries, such as the Netherlands and Belgium,

only three and half a full-time equivalent staff,

respectively, has been assigned to EUTR enforcement.

ItˇŻs noted that while big EU companies started developing

due diligence (DD) systems at an early stage - which had

sometimes resulted in a significant reduction in their

number of suppliers - and were ready to exercise DD when

the EUTR came into force, the vast majority of companies

across the EU applied a ˇ°wait and seeˇ± mentality.

Unless there is effective implementation, control and

prosecution on the one hand, and sufficient and clear

guidance on the other, especially the SMEs seem unlikely

to change their practice.

EUTR beginning to change trade practices

Nevertheless, the report suggests that EUTR is beginning

to change trade practices in those countries where

implementation is more advanced.

Specific changes identified include: increased awareness

on risk of illegal timber; increased import of certified

timber and a push to certification in some producer

countries; positive influence on legislation in producer

countries; and some benefits emerging for legal producers

due to exclusion of low priced illegal timber from the

market.

To some extent these benefits are offset by negative

changes including an increased cost and administrative

burden on operators, the withdrawal of SMEs in producer

countries from export markets, and confusion and

concerns in producer countries due to the lack of

harmonised implementation across EU countries.

The findings and recommendations of the report will now

guide the EC in improving the efficiency, effectiveness

and value-for-money of work undertaken to further

implement the Action Plan. The report will also guide the

EC in assessing policies to address the broader drivers of

deforestation, and in linking action under FLEGT to the

international climate change and Sustainable Development

Goals agendas.

Further details including a complete copy of the reported is

available at: http://www.euflegt.efi.int/eu-flegt-evaluation

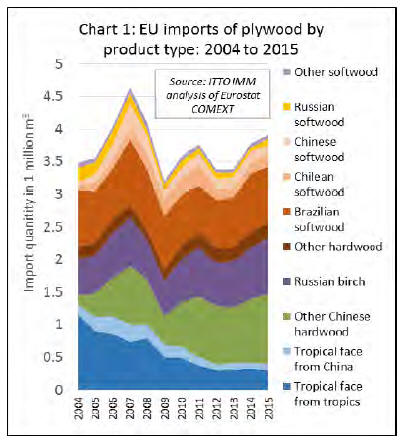

Tropical plywood share falls to all time low in EU

Latest EU import data shows that tropical plywood has

continued to lose share in the EU plywood market over the

last two years.

While EU imports of plywood from all sources increased

sharply between 2013 and 2015, from 3.38 million cu.m to

3.92 million cu.m, a level not seen since before the

financial crises, imports from the tropics have remained

stubbornly low (Chart 1).

After increasing 4% to 324,000 cu.m in 2014, EU imports

of plywood from tropical countries fell back 6% to

305,000 cu.m in 2015. The share of tropical countries in

EU plywood imports fell from 9.2% in 2013 to only 7.8%

in 2015, the lowest level for at least the last 20 years, and

probably much longer.

The share of imports of tropical hardwood faced plywood

from China also fell in the last two years, from 3.0% in

2013 to 2.4% in 2015.

Tropical hardwood faced plywood has lost share mainly to

Chinese plywood faced with temperate hardwood

(including poplar, eucalyptus and birch), and to Russian

birch plywood.

EU imports of temperate hardwood plywood from China

increased from 986,000 cu.m in 2014 to 1.07 million cu.m

in 2015 and share of imports increased from 26.1% to

27.2%. Over the same period, EU imports of Russian birch

plywood increased from 782,000 cu.m to 863,000 cu.m

and share increased from 20.7% to 22.0%.

Further gains by Russia and China in the EU market in the

last two years are likely due to the combined effects of the

weak Russian rouble, declining value of the Chinese yuan

and falling domestic demand in China, and rising

availability of plantation wood from China.

Weakness of the euro against the dollar during 2015 will

also have reduced sales of South East Asian plywood in

the EU.

Early indications are that the share of tropical countries in

EU plywood supply has continued to erode during 2016.

EU imports of plywood faced with tropical hardwood

were up 3.7% in the first three months of 2016 compared

to the same period last year.

However, this was largely due to a 38% rise in EU imports

of tropical hardwood plywood from China, from 23,700

cu.m in the first quarter of 2015 to 32,600 cu.m during the

same period in 2016.

So far this year, China has been the EUˇŻs largest supplier

of tropical hardwood plywood (Chart 2).

Imports from Malaysia were down 5.4% at 29,000 cu.m in

the first quarter of 2016 and imports from Indonesia

remained static at 28,400 cu.m.

Of significant suppliers in the tropics, only Gabon

registered an increase in exports to the EU in the first three

months of 2016, with a gain of 37% to 10,000 cu.m

compared to the same period in 2015. The latter is a trend

worth watching as perhaps signalling the first sign of

growth in the EU market for African okoume plywood

after many years of recession.

The gain in EU imports of plywood from Gabon in 2016

has been concentrated in Italy and the Netherlands, with a

much smaller gain in France where trade in this product is

still very limited.

The increase in EU imports of tropical hardwood faced

plywood from China this year has been concentrated

mainly in the UK and Netherlands (Chart 3). This is

notable from the perspective of EUTR and forest

certification, since importers and EUTR authorities in both

countries are renowned for their relatively rigorous efforts

to ensure wood is risk-free from an illegal logging

perspective.

This implies that a significant proportion of this material is

faced with certified tropical hardwood, or at least that

Chinese manufacturers are now successfully reassuring

customers of the legality of their tropical veneer supplies

by other means.

Another notable trend in the first quarter of 2016 was the

low level of import of tropical hardwood plywood into

Belgium, at 9,400 cu.m, less than half the same period in

2015. Belgian imports of plywood from Indonesia have

been much slower in 2016 than in 2015, although the fall

in Belgium has been offset by rising Indonesian exports to

the UK, Netherlands, Italy and Germany in 2016.

|